This report estimates the effect of the Nordic ecolabels on apartment buildings, canteens and laundry detergents in a Danish context. The report is proprietary and therefore not available on-line. The study was commissioned by Ecolabelling Denmark.

Denne analyse viser sammenhængen mellem en kommunes samlede indkøb fordelt på forbrugsområder, og den miljømæssige påvirkning dette forbrug medfører. Analysen viser en tydelig forskydning mellem den økonomiske og miljømæssige fordeling. I særdeleshed forbrug af transport, energi og fødevarer har en høj miljøbelastning set i forhold til deres økonomiske volumen og er derfor oplagte fokusområder i en kommunal klima- og miljøindsats. Det offentlige køber en lang række produkter og services for at kunne levere ydelser til borgerne. Alle disse produkter og services skal produceres, transporteres, anvendes og sidst bortskaffes. I hvert led i kæden påvirkes miljøet i højere eller mindre grad. Da det offentlige samlet set er den største indkøber i Danmark har offentligt indkøb i sagens natur også en stor indvirkning på miljøet. Offentligt grønt indkøb har længe været på dagsordenen i en lang række kommuner og statslige institutioner, men der har manglet et samlet overblik over hvilke typer af indkøb, der har den største indvirkning på miljøet. Denne analyses formål er at skabe dette overblik i en kommunal sammenhæng. Dette overblik kan bruges i Miljøstyrelsens videre arbejde med at udforme vejledninger i grønne indkøb og kan bruges i kommunernes arbejde med at prioritere miljøindsatser. Odense Kommune er anvendt som pilotkommune i projektet. Det samlede overblik over kommunes miljøpåvirkning opnås ved at lave et miljøregnskab med udgangspunkt i kommunens indkøb. I miljøregnskabet medtages produkternes fulde påvirkning fra produktion, brug og bortskaffelse, altså fra et livscyklusperspektiv. Derved fås et billede af kommunens såkaldte miljømæssige fodaftryk. Miljøregnskabet er udarbejdet med udgangspunkt i Odense Kommunes økonomiske regnskab for afrapporteringsåret 2010. Regnskabet dækker over de indkøb, der sker i kommunen som virksomhed, og altså ikke de aktiviteter, der sker i kommunen som geografisk område. Regnskabet er blevet sorteret og fordelt i henhold til 11 forbrugsområder. Den økonomiske fordeling på områderne er vist på Figur 1. Odense Kommune er anvendt som case, men kommunens indkøbsmønster kan angiveligt sidestilles med indkøbet i mange andre kommuner. Miljøregnskabet kan derved hjælpe med at udpege indsatsområder for alle kommuner med særlig fokus på indkøb samt anvendes til prioritering i den nationale indsats for at fremme offentlige grønne indkøb. Baggrundsdata findes i tilknyttet metoderapport.

The Environmental Profit & Loss account (E P&L) results was used to evaluate Arla Food’s environmental strategy 2020 in order to assure that its focus was in the ‘right’ areas. The E P&L was also used in various communications and was an important step to show that Arla Foods takes its environmental work seriously and take responsibility for the whole value chain.

The project was part of the increased focus of the Danish government on Natural Capital Accounting (NCA) as a way for companies to report their environmental impact. Arla had chosen to go further than just natural capital impacts and extend the study to a full EP&L study covering also other environmental impacts (see also our blog-post about the terminology of EP&L versus NCA). At that time only a few companies had conducted EP&Ls or NCAs and Arla Foods was the first food company to conduct such a study.

The unit of analysis was the sum of all Arla Foods's activities in 2014. Hence, the E P&L included all environmental life cycle impacts from cradle to grave of the sum of all Arla Foods’s products for the financial year 2014. This involved emissions and resources involved in the production of raw milk at farm level, transportation, processing in Arla Foods’s manufacturing facilities, distribution, retail, consumption and disposal.

The E P&L included activities for the whole company, including the daughter companies Arla Foods Ingredients, Rynkeby and Cocio, but excluding joint ventures. All Arla foods production sites (77 sites in 12 countries) were part of the study, together with inbound and outbound transport, and packaging. Production and use of raw materials, energy carriers, etc. were included, as well as management of by-products and waste materials. Also products and services not directly used in production, such as computers, furniture, travels, etc. were covered. The downstream part of the supply chain (retail and consumers) was also included in the E P&L.

To obtain a comprehensive understanding of the full environmental impact of Arla Foods, the following environmental impact categories were included; global warming, eutrophication, acidification, other air pollutants (e.g. particulate matter, PM10), energy use, water use, resource depletion (e.g. phosphorus), waste, land occupation, biodiversity. Each of these impacts were valuated/monetarised in order to also show the results in monetary units.

The project was reported in the report Arla Foods Environmental Profit and Loss Accounting 2014.

The E P&L accounting model has only been conducted for companies so far, and the companies that have applied the model have usually been large and resourceful. A key question of this project was “How can small and medium sized companies as well as other stakeholders take advantage of this new methodology of quantifying and valuing natural capital throughout the value chain?”

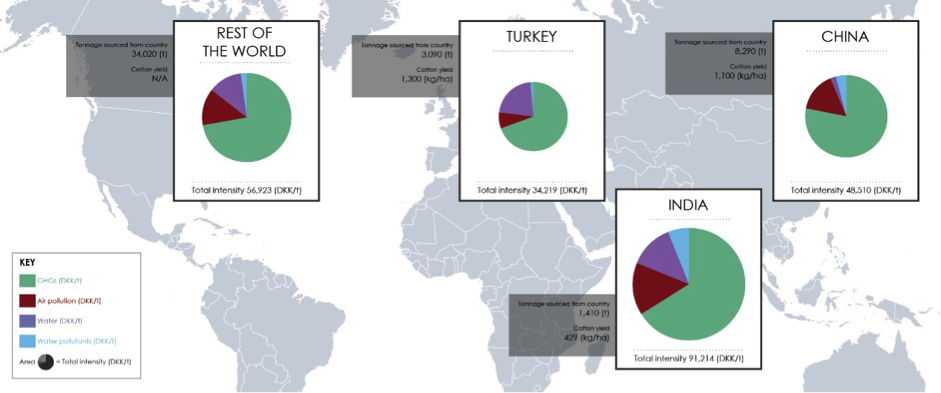

An E P&L conducted at the country consumption level could benefit a wider group of stakeholders, including trade associations, government bodies and the companies in the industry. More specifically, the E P&L for Danish apparels gives an overview and a complete picture of the environmental impacts related to suppliers throughout the value chain. The E P&L at this level also illustrates the relationship between what is emitted domestically and internationally. In addition, the E P&L provides information on how the Danish apparel industry works compared to other countries. On a company level, the E P&L contributes to understanding the environmental profile of different industries in the apparel supply chain, and provide useful insight to the companies on where the risks and opportunities are in the value chain. Finally on a product level the E P&L can provide a more precise product profile and illustrate the impact of substituting conventional materials with more sustainable alternatives.

The objective of this project was therefore to conduct an E P&L analysis across three levels:

1. Industry level (relevant for trade associations and government bodies)

2. Company/brand level (relevant for trade associations and companies)

3. Product level (relevant for trade associations and companies)

The results from the project can be found in the report: Danish apparel sector natural capital account.

Figure – Impact intensity for all countries of import (all tiers)

Carbon footprint is a new buzzword that has gained tremendous popularity over the last few years, especially in the United Kingdom.

Debates on the appropriate use of carbon footprinting are spreading through society like rings in the water. This in large part has been driven by retail chains and proactive companies that request or provide information to the consumers for example, for the purchase of airplane tickets and carbon offsets.

.....

The first contribution was a presentation to the Life Cycle Management Workshop of the UNEP/SETAC Life Cycle Initiative in Johannesburg, 2002, entitled Quantifying Corporate Social Responsibility in the value chain. An important message here was the relevance of the ISO 14040-series for Social LCA a point that was iterated in a 2005 Letter to the editor entitled ISO 14044 also applies to social LCA.

The contribution to the quantification of social impacts was carried one step further in the 2005 conference presentation and the journal paper with the title The integration of economic and social aspects in life cycle impact assessment and the 2006 presentation Social impact categories, indicators, characterisation and damage modelling to the 29th Swiss LCA Discussion Forum.

As vice-chair of the UNEP/SETAC cross-cutting "Task Force on Social Aspects in LCA", Bo P. Weidema contributed to the 2006 feasibility study and the final 2009 Guidelines for Social Life Cycle Assessment of Products and the accompanying Methodological Sheets.

This work is currently continued in our LCSA club.

Common roots of CBA and LCA

Cost-benefit analysis (CBA) and life cycle assessment (LCA) share the objective to provide holistic, ex-ante assessments of human activities, and both techniques have developed from engineering practice. In spite of this common objective and the common roots, CBA and LCA have developed in relative isolation. This has resulted in a situation where much can be gained from an integration of the strong features of each technique. Such integration is now being prompted by the more widespread use of both CBA and LCA on the global arena, where also the issues of social responsibility are now in focus. Thus, it is time to sketch a common frame of understanding of environmental externalities. Such a common frame is provided by the conceptual structure of life cycle impact assessment (LCIA) developed by within the SETAC/UNEP Life Cycle Initiative (Jolliet et al. 2004).

.....